Tax the seed or the harvest... or neither?

Perhaps it is my upbringing in agriculture or my love of daylight savings time (yes I lost an hour, but it’s lighter later!), but this post will describe the differences in tax-qualified vehicles (think 401ks/403bs, IRAs, HSAs, 529s) in terms of growing things. IRAs are topical as the tax filing deadline nears. For my newsletter subscribers, see the March issue for a handy reference to different contribution and deduction limits based on income for various accounts called “2016: Important Tax Facts for Investors.”

With a crop, you plant a small seed in the ground, patiently care for it while natural laws prevail, then harvest the bounty at the end. For the connection to tax-qualified accounts, the seed is the contribution, growth is investment gains and harvest is the withdrawal. And in the spirit of “If it moves, tax it…” you have to pay taxes somewhere for most accounts.

All tax-qualified accounts don’t incur taxes during the growth phase. The difference is whether taxes are paid based on the contributions going in (the seed) or the withdrawals from the account (the harvest). Roth 401ks/IRAs have contributions from funds already taxed, the account grows tax-free and funds withdrawn are not taxed – i.e. the seed is taxed. Traditional 401ks/IRAs have contributions from pre-tax funds, the account grows tax-free and funds withdrawn are taxed as ordinary income at the time withdrawn – i.e. the harvest is taxed. Note I said ‘taxed as ordinary income’. Currently the long-term capital gains rate (investment growth held for more than one year) is taxed at 0%, 15% or 20% depending on income levels; the ordinary income tax rate is higher for each corresponding level. This means some investors are converting investment growth into a higher tax rate when withdrawn.

The first step is to determine which accounts are allowed and if contributions would be deductible based on income (applies to IRAs, not 401ks). Then the main deciding factor is the expected tax rate when contributions are made versus funds withdrawn. If your tax rate is expected to be lower during retirement, you may choose to use a Traditional 401k/IRA which allow deductible contributions and then taxes are paid on withdrawals while in a lower tax bracket. If you expect to be in the same tax bracket, it is economically a wash. Yes you get to delay paying taxes, but you must also pay taxes on all that growth. However, you do have access to those funds now which may be appealing for those with a high utility value of money. That is a fancy way of saying you may value an extra dollar in your pocket when funds are tight versus the same dollar when you have excess funds and are looking for more savings opportunities.

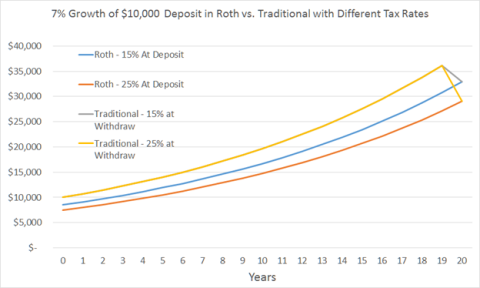

That is a lot of words. I think it’s time for a picture. The graph below shows the growth of different accounts for different combination of tax brackets when deposit and withdraw. Note the Traditional IRA has the same balance until the end when driven by different tax rates. For simplicity, I assumed the Traditional IRA withdrawal occurs at once. In reality it occurs over time but the economics are the same provided in the same tax bracket.

There are other considerations and tax nuances that should be considered but not addressed here:

- Must consider both Federal and State tax rate

- You may live in a different state during retirement; not only will the rate be different but some states exclude IRA withdrawals from taxes

- Tax laws can change at both the Federal and State level

- Depending on income, extra taxes may apply in the decision like the extra ‘Medicare tax’ of 3.8%

- Roth accounts have additional advantages, like access to principal without early withdrawal penalty and no required minimum distributions

Finally, there are two types of accounts that have taxes minimized further:

- A 529 college savings plan is similar to a Roth except some states allow a state tax deduction on contributions up to a certain limit. Withdrawals must be used for qualified education expenses.

- A Health Savings Account (or HSA) doesn’t incur taxes at any of the three phases, provided withdrawals are used for qualified expenses. This should not be confused with a health spending account or some other similar sounding name where you get a deduction but must “use it or lose it” each year. Think of these accounts as a medical IRA that allow tax-free contributions, the account grows and withdrawals are tax-free provided used for qualified medical expenses. The other requirement is you need to have a qualified high deductible medical insurance, called an HDHP account. You may also find the high deductible insurance policy, which requires you to pay more of your medical care in exchange for lower premiums, forces you to be aware of the true cost of different medical visits and procedures. This will likely make you a better consumer of medical care, like every other item you purchase with your hard-earned dollars, helping to keep overall medical costs in check.