Should I Open a Trump Account?

Trump accounts were introduced in the One Big Beautiful Bill Act (OBBBA) last July and will become operational this year. These are like IRA accounts for kids. Any child with a Social Security number can have an account opened on their behalf (a custodial account - adult handles) provided they are under the age of 18 at the end of the year the account is opened. What gets the most attention is the Treasury will contribute $1,000 into accounts for children born between 1/1/2025 and 12/31/2028. Some individual donors have also announced programs with a $250 contribution using certain criteria that can apply to children born before 1/1/2025 but after 1/1/2015.

Should I set one up? What are the rules? Are there better alternatives? All good questions. If you qualify for the “free money”, it probably makes sense to establish an account and receive the funds. Whether it makes sense to add your own funds will depend on other considerations. Read on for more details in a Q&A format.

Q1 – Who is eligible to open an account and how is that done?

Any child with a Social Security number (SS#) who is under the age of 18 at the end of the year can have an account opened. Not all these accounts will receive contributions from Treasury or individual donors. The program will launch July 4, 2026 but you can begin the account opening process now in one of two ways:

- Go to trumpaccounts.gov and complete Form 4547 electronically, or

- Complete Form 4547 with your tax return.

You will be notified later which custodian will handle the accounts and steps to complete the account setup. If eligible, contributions should automatically be deposited when the program officially begins.

Q2 - Who qualifies for the $1,000 from Treasury? Are there additional donor programs with $250?

Children born between 1/1/2025 and 12/31/2028 with a valid SS# are eligible to receive $1,000 into a Trump account if opened. There is no limit to the program on how many children can claim. In addition, some companies and individual donors may also add additional amounts (individual donors’ programs announced are for $250) to a broader group of children.

- Some employers may match the Treasury contribution for their employees which implicitly means limited to same criteria – mainly born between 1/1/2025 – 12/31/2028.

- Individual donors Michael and Susan Dell have committed $6.25 billion to fund up to 25 million accounts with $250 for children 10 and younger born before 1/1/2025. This is a national program and further limited to zip codes where median income is below $150,000. It appears there is no individual income limit.

- Individual donor Ray Dalio announced a program with similar criteria as the Dell program but for children born in Connecticut. This program is structured as matching the Dell grants, so Connecticut residents could receive $500 if meet the criteria.

- Watch for additional programs, including state specific like Dalio, that may develop since donors know that 100% of their donation will start in the Trump account helping the future minds of our nation with minimal expense ongoing. That direct connection of where charitable contributions are going and how they will be utilized can be attractive.

This reminds me of a quote in the book Millionaire Next Door by a no-frills guy who was invited to a reception by the author and was asked what he wanted to drink: “I like two kinds of beer – Budweiser and free.” Take the free!

Q3 – Can I or others put additional amounts into the accounts? How much per year?

Yes, but whether you should depends on other considerations covered later. In addition to any government or individual donor contributions, up to $5,000 per year can be added from parents, relatives or friends. Employers can contribute up to $2,500/year but that is part of the $5,000/year limit. Note these contributions can occur even if the child has no income (unlike a minor IRA for example). Also note these contributions must stop at age 18.

Q4 – What are the investment options for Trump Accounts?

It is limited by design to keep expenses low and investments diversified within the US equities (not a true portfolio diversification). The investments will be limited to a low-cost mutual fund or exchange-traded fund with an expense ratio at or below 0.10%. While this may be a solid choice for long-term investors, it will be very limited as the time horizon shortens, say as the child is approaching college. There may be changes to the program over time. This would be a very important change to make in my opinion so that risk could be dialed down as the time horizon shortens depending on the use of the funds. It doesn’t have to be many choices – maybe similar to the Thrift Savings Plan (TSP) for government employees which has only five choices – but at least a choice.

Q5 – Do these accounts end at age 18 or can they continue longer?

They definitely can go longer, but you generally can’t access the funds before age 18. As noted above, new contributions must also stop at age 18. There are limited exceptions like death of a child or converting to ABLE accounts for a disabled child at age 17. But assume can NOT access, even if an emergency, before age 18. At age 18 you can continue letting the accounts grow tax-deferred into retirement if wish, or begin withdrawing funds for different purposes, but some withdrawals may have a 10% penalty, in addition to taxes (sounds like an IRA, right?). You are NOT allowed to roll these into a Traditional IRA. More details about the restrictions and tax treatment will be covered below.

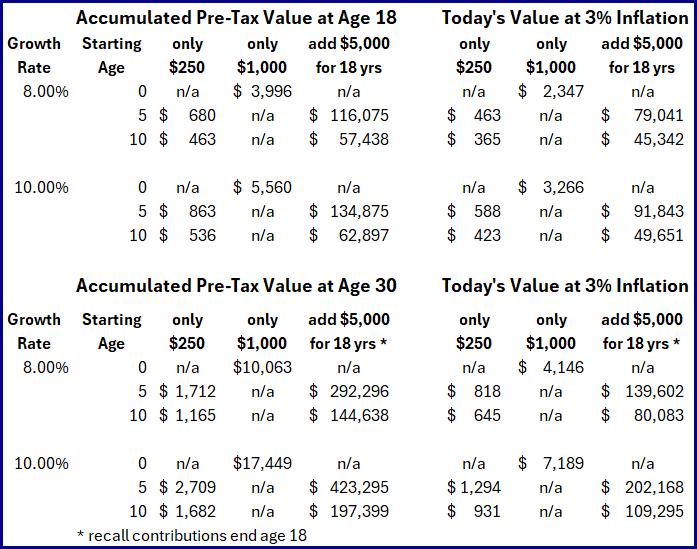

Q6 – How large could these accounts grow? Is it worth it if only plan to take the $250 deposit?

More than you think. Here is a table showing the potential growth of these accounts at age 18 and age 30 (accounts can go longer if wish) for different starting ages, contribution amounts and investment returns. I also discount the ending value back using 3% inflation to see the purchasing power Junior/Juniorette would have. That could be a nice computer, a flying car to get to class (or whatever developed by then!), or a down payment on a house.

For those old enough to remember, this is similar to the EE Savings Bonds that a relative may have purchased at the birth of a child. It may seem like a modest amount at the time but that 18-year-old is happy to see the accumulated value. These accounts have the ability to grow even larger (but also fall in value!) since invested in a diversified equity fund.

Note these are pre-tax dollars. My next few questions will cover tax treatment.

Q7 – Is the contribution deductible? Are Treasury or individual donor amounts taxable?

No to both, at least on the way in. Contributions from Treasury or individual donors are not considered as taxable income in the year contributions made but will be taxed when withdrawn (covered later). A contribution made directly by an individual is not deductible but rather made with after-tax dollars. However, it appears an employer could set this up through a Section 125 cafeteria plan where the employee could then contribute with pre-tax dollars – but only to a dependent’s account with max of $2,500. That would be an interesting development to watch and definitely change the consideration for adding your own contributions.

Q8 – What is the tax treatment while funds grow and later when take withdrawals? Is there an early withdrawal 10% tax penalty?

The accounts would grow tax-deferred. Because the investment would be limited to likely an index fund and no ability to trade (only one investment choice now), there would be no ability to generate capital gains and the considerations of short- vs. long-term gains. This actually makes some of the existing alternative account choices more attractive which I will discuss later.

No withdrawals can occur before age 18. At that time, the child then becomes the account owner and can do what they wish with the account. Yes let me state that again, at age 18 the account is now owned by the child who controls it as they wish (some state laws with majority age of 21 may vary, not sure).

In general, the withdrawal tax impact will be treated similar to a Traditional IRA. Withdrawals would be taxed as ordinary income using the account owner’s tax brackets on all investment gains and any pre-tax contributions, including the initial seeding if applicable from Treasury and individual donors. Similar to Traditional IRAs, funds withdrawn before age 59.5 are also subject to a 10% penalty (ouch!) unless the withdrawal meets one of the exceptions (here is list from the IRS). Common exceptions (some with maximum amounts) include birth/adoption of child, disability, disaster, higher education (but not room/board!), first time home buyer, certain medical if above 7.5% AGI, and others.

Q9 – What are some existing alternative accounts that could be used instead of Trump Accounts?

There are plenty – but only when considering new contributions. The only way to get the Treasury or individual donor funds is to open a Trump Account. Remember, take the free (and you may want a Budweiser if still reading this far down!). I will list a few accounts with brief bullet point considerations vs. a Trump Account (TA).

529 College Savings

- Some states allow state tax deduction on contributions – TA NO

- Same tax-deferred growth BUT no tax on 529 withdrawal if used for qualified education expenses – TA are taxable (though 10% penalty waived)

- More investment flexibility to dial down risk as college approaches – TA only 100% US equities

- Withdrawal flexibility before college age if need (with tax and penalty implications) – TA NO

- Funds can be used for other qualified expenses beyond tuition and in years K-12 – TA only higher education for tuition

- Excess funds can be used for different beneficiary or up to $35k transferred to Roth (subject to rules) – TA NO

Custodian Taxable Brokerage Account

- No deduction on contributions – TA same

- Must pay tax on investment income and capital gains while grows but likely a portion more favorable with the kiddie tax – TA NO

- Full flexibility with investment choices – TA only 100% US equities

- If managed properly, investment gains at favorable capital gains rate – TA as ordinary income

- More flexibility on withdrawals and timing, though for benefit of child – TA only after age 18

Minor IRA – likely a Roth given low deduction benefit of Traditional for child

- No deduction nor tax while growing, but Roth comes out tax-free – TA taxed ordinary income

- Child must have ‘taxable compensation’ in order to contribute – TA no income required

- Full flexibility with investment choices – TA only 100% US equities

- More flexibility on withdrawals, especially direct contributions that can be withdrawn any time without tax or penalty (investment earnings a different story) – TA only after age 18; some 10%

Q10 – Bring it home… what are your concluding thoughts?

My initial reaction was to open a Trump account if child born between 1/1/2025 and 12/31/2028 for the free $1,000, otherwise don’t bother. With the new individual donor programs being announced, it now makes sense if child is below age 10 AND live in a zip code with median income below $150,000 (more areas than you would think, so check).

Another area to watch is employer programs. The ones announced so far involve matching the Treasury contribution so by definition, only for those in the four-year birth window. However, if employers also include Trump Accounts funding as part of a Section 125 cafeteria plan with potential pre-tax contributions (up to $2,500) that could get interesting.

So other than that, why would you use them? If you have tapped out all your own tax qualified savings vehicles and the ones available for a child and you want to do more to jump start retirement savings – go for it. Just remember the investment and withdrawal limitations, and Junior/Juniorette gets full access to the funds at age 18 (or maybe 21 in some states, not sure).

A few more random thoughts based on past reading and podcast listening (at 2x speed!). Also note “Rome wasn’t built in a day” - it is easier to start small to push across the finish line, then enhance once something up and running. Don’t let perfect get in the way of good. Trump Accounts are good.

- I do believe will have increased individual donors’ involvement since a well-defined program going directly to the young minds of our nation, rather than some “government program”

- I do expect investment choices and ability to dial down risk to increase as that is a major shortcoming if planning to use funds shortly after age 18

- As of now, I believe Trump Account would be considered child’s asset for college aid funding; that could change; still ok for the “free money” portion, but ponder for additional funding

- I mentioned full access to funds at age 18 a few times already; Marc Fabor had a comment on a recent podcast where he has seen funds pulled from these types of programs once able to if come across near-term hardship and lose the long-term benefits

- Could this be considered a trial balloon for part of the solution to Social Security funding crisis our nation faces? Similar ideas to invest part of SS funds in equity market or individual accounts have been floated in the past

- The potential for another government bailout since politicians can’t help themselves. Picture down the road when a large US market drop and some Trump Account holders see large losses that they were planning to use for college. Surely the politicians will bail me out, right? Right?!

There you have it. My summary of Trump Accounts. There was a lot more here than I expected when I started writing this blog. And while I still believe “take the free money but don’t add more” generally applies, the new individual donor programs and employer actions – and potential program changes - bears watching to refine your analysis and considerations. Now where’s my Budweiser - and how is my bracket doing?

Have questions? Reach out! We're happy to help.

Posted by Kirk, a fee-only financial advisor who looks at your complete financial picture through the lens of a multi-disciplined, credentialed professional. www.pvwealthmgt.com