Key Lines from 2025 Tax Return for 2026 Planning

Your 2025 tax return has likely been filed and you have the electronic or paper copy from the accountant or tax software. Before tossing in your files, review the return and engage in tax planning for 2026. This blog post will identify key lines and highlight common strategies to employ now for a favorable tax return next spring. As a reminder, this is not formal tax advice (I am not an accountant) but rather background information to help with planning. This is also not a comprehensive list of all tax strategies available.

I will focus on Federal taxes only using the two-page Form 1040 summary. I may reference a few supporting Schedules and Forms but much information can be gleaned from these first two pages of your return. Before jumping into Form 1040, here are a few key concepts to help understand the tax return.

- Two different types of income:

- ordinary income – wages, IRA withdrawals, part of SS and annuities, bond interest, non-qualified dividends, short-term capital gains, RSUs, options

- capital gains –qualified dividends, securities or property held more than 365 days

- Deductions that reduce taxable income

- Part II of Schedule 1, like IRA and HSA contributions

- Itemized on Schedule A or Standard, Senior Deduction, Qualified Business Income

- Which deductions impact different income definitions

- Deductions on Schedule 1 impact Adjusted Gross Income (AGI) and various definitions of “Modified AGI”

- Itemized or Standard, Senior, QBI and others lower taxable income but not AGI

- Income less deductions results in taxable income, but different tax rates apply

- Shows total ‘taxable income’ but ‘ordinary income’ and ‘capital gains’ run through different tax brackets by income.

- Tax brackets by type – Single, Married Filing Jointly, Head of Household, Trust

- Extra 3.8% Medicare tax to ‘investment income’ – both ordinary + cap gains

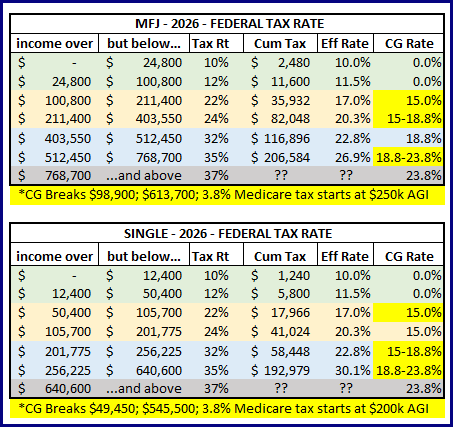

- Below are the Single and Married Filing Jointly tax brackets for 2026 tax year

Below is an actual Form 1040 from 2025 with key lines to discuss circled in red. I will list two bullet points for each: first - a brief explanation of the number; and second - some strategies to impact your 2026 tax return next spring. I will add a third bullet if impacted by the new tax bill OBBBA (recent blog post summary), SECURE Act or other recent changes. There are many complexities behind each so I will only highlight the strategies, not provide all the details. Reach out for help. Some of the lines identified may have $0 in this return but may apply to your situation.

Form 1040 – bottom of page 1, top of page 2

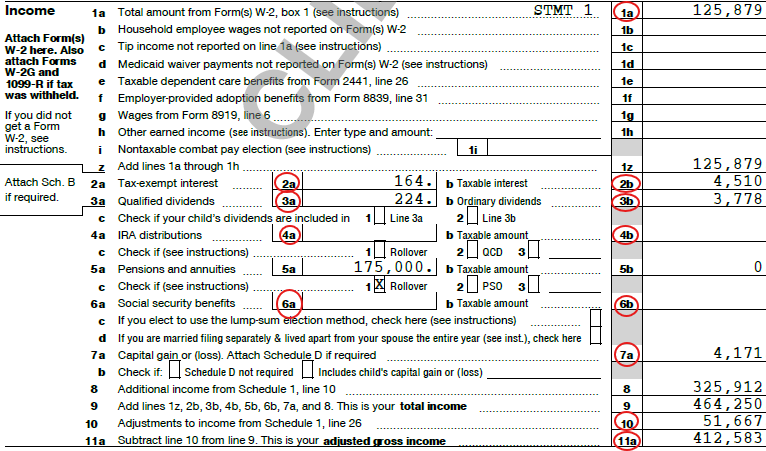

Line 1a – W2 income

- Wages from employment reduced by tax-deductible savings from payroll like Traditional (not Roth) 401k, Health Savings Accounts or Flexible Spending Accounts.

- Since there is no income limit on using these savings accounts for deductions, if in higher tax bracket be sure to max out these savings vehicles.

- NOTE: SECURE Act 2.0 finally implementing age 50+ catch-up contributions must go to Roth 401k if ’25 income (W2 Box 3) from same employer above $150,000.

Line 2a, 2b – Interest, both tax-exempt (a) and taxable (b)

- Interest earned from bank savings and bond holdings; this number is higher in recent years due to higher interest rates

- Bond income treated as taxable ordinary income unless municipal bonds which are tax-exempt (mostly); important to compare the pre-tax yield equivalent of muni’s - based on marginal tax rate include Medicare tax – to a taxable equivalent bond.

Line 3a, 3b – Dividends, both qualified and non-qualified

- Dividends paid from equity holdings like ETFs, mutual funds and individual stocks.

- Qualified dividends are taxed at long-term capital gain rate so be aware of which ETFs kick of qualified dividends (most do except REITs); if asset allocation and location forces choice, hold dividend paying equities over non-muni bonds in taxable account.

Line 4a, 4b – IRA distribution, both total withdrawn (a) and amount taxable (b)

- Total distributions listed in Line 4a withdrawn from Traditional IRAs/401ks from 1099-R, typically the amount needed to satisfy the required minimum distributions at older ages but also where regular withdrawals and Roth conversion amounts are captured.

- Not all withdrawals are taxable; two common exceptions are after-tax basis in IRA (see Form 8606) or Qualified Charitable Distribution (QCD; if 70.5 or older and give directly to charity). Consider partial Roth conversions if in lower bracket but watch out for impact on other tax lines, especially SS, IRMAA, and OBBBA impacts!

- NOTE: Starting in 2026 custodians are required to enter code on 1099-R indicating some QCDs. Be sure to verify and still provide amount of QCDs to accountant.

Line 6a, 6b - Social Security benefits

- Gross amount received is on Line 6a BEFORE Medicare premium deductions or tax withholdings. The taxable amount on Line 6b is based on something called “provisional” income. If that number is above $34,000 for single filers or $44,000 for joint filers (NOT indexed for inflation – will get us all!), a portion of gross benefits will be added to your taxable income.

- The portion of SS benefits included in taxable income can range from 0% to 85% depending on above levels; if fortunate to be below 85%, be aware of the “tax torpedo” triggered by other actions like Roth conversions or realizing capital gains which will force a higher % of SS to be taxable.

- NOTE: OBBBA did not exclude SS benefits from income but did include a $6,000 Enhanced Senior Deduction, subject to income limits (see Line 13 below).

Line 7 – Capital gain (or loss)

- Gain or loss realized from selling security; if held 1 year or less considered “short-term” and subject to higher ordinary income rates.

- Be aware of short- or long-term status and marginal capital gain tax rate at 0%, 15%, 18.8% or 23.8% (yes, 4 long-term rates and some at 0% - can harvest gains) or at the always higher ordinary income rate. Losses can offset gains. If losses dominate, up to $3,000 can offset ordinary income; unused losses can be carried forward indefinitely for individuals to offset future years’ gains.

Line 10 – Adjustments to income

- Look at Part II of Schedule 1 for the various deductions used to reduce taxable income (if qualify; many have income or other limits). Some can be funded in first few months of the following tax year before filing taxes like IRA and HSA contributions.

- The types of deductions range from Health Savings Accounts (if high deductible plan, no income limit), Traditional IRA contributions (if income low enough), retirement plans for self-employed (Individual 401k anyone?!) or interest on student loans (income limits).

Line 11 – Adjusted Gross Income (AGI)

- This is a calculation capturing the numbers above, sometimes called “above the line” since before itemized or standard deductions. This is a very important number since many credits and eligibility for deductions reference this number or a close “Modified” variation. Be aware there are many definitions of “Modified Adjusted Gross Income (MAGI)” depending on the deduction or credit looking at!

- You may think there are no strategies to employ since a calculation, but your strategy is to be aware of which deduction, credit or other items are dependent on a particular MAGI definition and revisit the lines above for strategies. Key items driven off of MAGI include extra Medicare premium triggers (IRMAA), IRA deductibility and new OBBBA.

- NOTE: many OBBBA features are income dependent including higher SALT deduction (see Line 12) and Enhanced Senior Deduction (see Line 13).

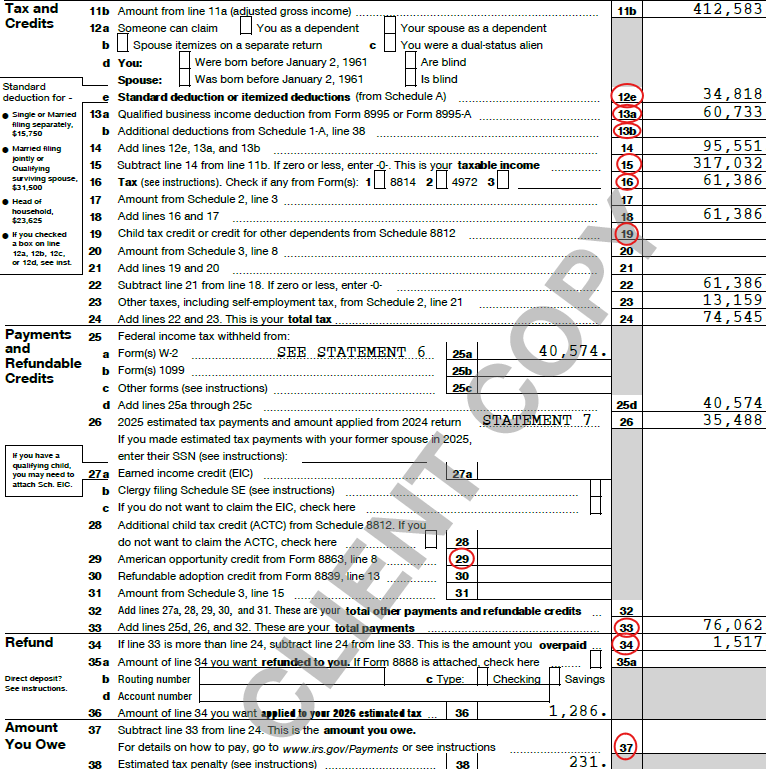

Line 12 - Deductions – standard or itemized

- AGI is reduced by a ‘standard deduction’ or ‘itemized deductions’ if higher (see Schedule A). There are additional components to ‘standard deductions’ if 65 or older – which is different than the Enhanced Senior Deduction.

- The ‘standard deduction’ was raised substantially in 2017 after state and local taxes (“SALT”) was capped at $10,000. This meant more filers used the ‘standard deduction’ and increased the value of QCDs (see Line 4b) and larger charitable donations via ‘lumping’ or use of Donor Advised Funds (DAF).

- NOTE: OBBBA changed charitable deductions in 2026 and expanded SALT up to $40,000 in 2025 (subject to income limits) so more filers may be itemizing again. Starting in 2026 can deduct up to $1k for Single; $2k for MFJ charitable contributions if use standard deduction; lose the first 0.5% x AGI of charitable if itemize.

Line 13a, 13b – Qualified Business Income deduction (QBI) and new special deductions

- There are additional deductions beyond Line 12. Line 13a applies for business owner or sole proprietor with either Schedule C or S-Corp income. Started in 2017 to replicate the lower corporate tax rate then approved. Line 13b was new in 2025 to capture the Enhanced Senior Deduction, TIPS, Overtime, Car Loan Interest (for special cases).

- This is an underappreciated business planning line for 13a as it adds extra complexity to Traditional vs. Roth decision on retirement plan savings (if chose 401k plan). Also has income limits so watch any Roth conversion impact.

- NOTE: OBBBA added special exemptions, including the $6,000 Enhanced Senior Deduction which is subject to income limits based on MAGI, so a new number to monitor while looking at partial Roth conversions and other tax planning.

Line 15 - Taxable income

- Amount of income subject to taxes after various deductions and exclusions – sometimes referred to “below the line” income since after deductions. You would think this is the amount to run through tax brackets but that would be incorrect, unless you have no capital gains or qualified dividends.

- There is a lot going on with this number. Two key items to be aware of: 1) know what portion is subject to “long-term capital gains rate”; and 2) know your marginal tax rate based on what’s left. You may have more room to realize capital gains or find a portion is taxed at 0% (see Line 7). The limits are ‘used up’ by ordinary income first before the more favorable capital gains amount is considered, which is difficult to explain so I will stop there!

Line 16 – Preliminary tax based on Taxable Income

- Calculation – many calculations actually – to arrive at total taxes due before credits and offsets.

- Unlike Line 11 there are no strategies here. All the work is done on the lines above.

Line 19 and 29 (and others!) – Different credits

- Direct $ offset to preliminary tax calculated in Line 16. There are many, and most have different income limits and requirements.

- Look at all of them. In addition to looking at income limits and controlling if possible on previous lines, the Line 29 credit also requires incurring a portion of education tuition expense with non-tax-qualified money (i.e. not paid from a 529 plan).

Line 33 – Total tax payments

- You control most of this number, either by properly filling out Form W4 with employer, making estimated tax payments up to four times a year or asking that taxes be withheld from IRA withdrawals (be careful with Roth conversions) or SS/pension payments.

- Read the next section, then take action to impact this number.

Line 34 or 37 – Refund or payment

- It is important to note the size of refund or amount you owe is NOT the only number that tells you if your tax bill is high or low. This is simply the end result of your planning.

- Ideally you should owe a little, but low enough to avoid penalties. There are ‘safe harbor’ amounts to pay and still avoid penalties. You should not rejoice if you received a large refund - that means you lent the government money throughout the year at 0% interest rather than using or earning for yourself.

Who said taxes aren’t fun? Ok, probably most people, but there is a lot of value to be picked up by understanding the key drivers. Happy tax planning … and call for help!

Have questions? Reach out! We're happy to help.

Posted by Kirk, a fee-only financial advisor who looks at your complete financial picture through the lens of a multi-disciplined, credentialed professional. www.pvwealthmgt.com