Dividend Payers in an IRA? Not Always.

Some experts recommend holding dividend paying stocks in a Traditional IRA rather than a taxable account. The ability to defer paying taxes on a high stream of income of which you have no control on the timing is the main reason cited. As a general statement, I disagree without looking at the investor's tax situation.

The main considerations centers around different federal tax treatment for qualified dividends vs. withdrawals from Traditional IRAs and state tax treatment of both. For clarity I am talking about individual stocks and equity ETFs whose dividends are qualified. Non-qualified dividend paying securities like REITs and bond interest payments are treated as ordinary income and are better held in a Traditional IRA over a taxable account under most circumstances. Traditional IRAs are mentioned here but this also applies to SIMPLE, SEP and Traditional 401ks. Roth IRAs and Roth 401ks have different treatment and analysis.

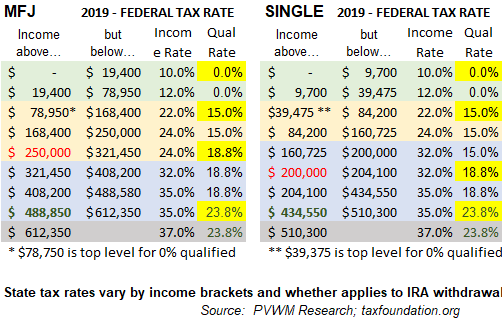

Most dividends from equities (excluding REITs) are treated as qualified dividends. These along with long-term capital gains are taxed at a lower rate, mostly 15% but can be as low as 0% (yes 0!) and as high as 23.8% (includes Medicare surcharge). Withdrawals from Traditional IRAs (with $0 IRA basis) are taxed as ordinary income, even if some or most of the withdrawal was generated from dividend payments or long-term capital gains. The ordinary income tax rate is always higher than the qualified dividend rate across different income levels. The table below summarizes the 2019 tax rates by income levels for 'married filing jointly' and 'single'.

Assuming the goal is to maximize the net after-tax dollars in a person’s pocket rather than maximizing a pre-tax account value that still has to run through the tax shredder, there are scenarios where you are better off paying the inevitable taxes sooner. For those old enough to remember, this is similar to the FRAM oil filter commercials when the mechanic states “you can pay me now, or pay me later.” Note this analysis is looking at where to hold the dividend payers in a portfolio if given the choice. A similar but different analysis is needed for Roth v. Traditional, Roth conversions and non-deductible Traditional contributions.

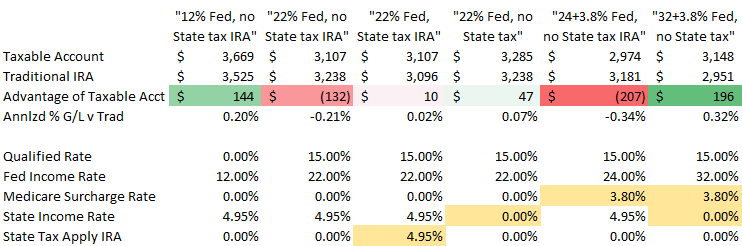

The examples below compare holding a $1,000 dividend paying stock with a dividend yield of 4% and price gain of 3% held for 20 years in a taxable account vs. a Traditional IRA. Six different scenarios are shown reflecting different tax environments individuals may face. The ending after-tax value is shown for each account type (IRAs apply tax rate at end of 20 years) followed by the difference in value and the annualized equivalent over the 20 years. The applicable tax rate is captured below. Unless you have a very high state tax rate, if in the 12% Fed bracket you should favor taxable; if in 22% it will depend on whether state taxes apply to IRAs and time before withdrawing (second scenario favors taxable for first 9 years). At the higher Fed brackets, the impact of Medicare surcharge and whether a state tax is applicable can swing the results.

This analysis assumes current tax law doesn’t change. If the difference between ending account values is small and you believe income tax rates may be higher in the future, then more scenarios will favor the taxable account. For example, if IRA withdrawals became taxable at the state level (or you move to a state that does) the advantage switches over to the taxable account for someone in the 22% bracket (third scenario below).

Simply stating you should hold dividend payers in a Traditional IRA does not correctly capture the optimal solution for all investors. Rather, perform the analysis or work with someone who can to determine which account type is best suited for different security types – with different tax treatment – in your overall portfolio.

Posted by Kirk, a fee-only financial advisor who looks at your complete financial picture through the lens of a multi-disciplined, credentialed professional. www.pvwealthmgt.com