Asset Class Returns - 12/31/2021

Here is this month’s market summary. Unless noted, the time frame is year-to-date with screen shots through 1/5/2022.

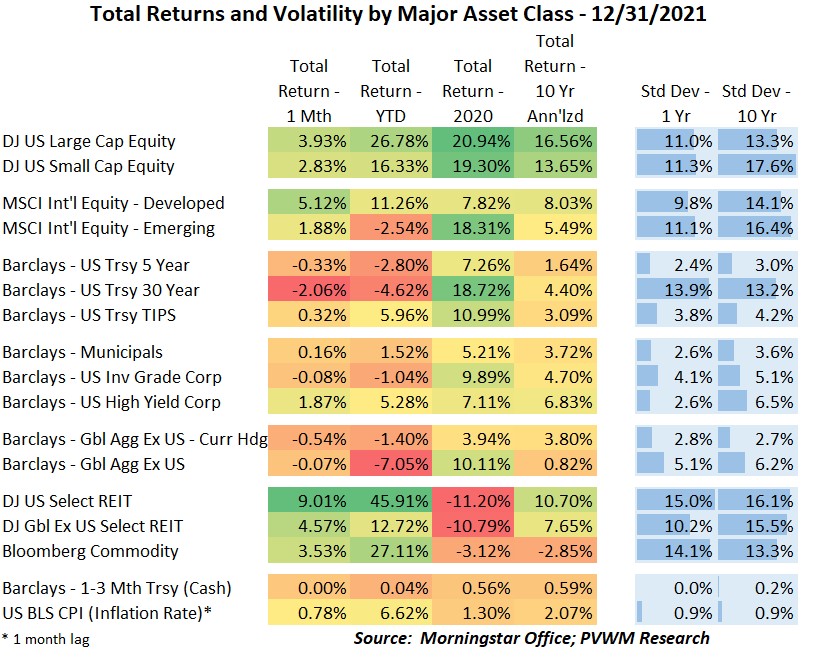

Most asset class returns meandered during the first half of December. The second half rally into year-end seemed to be a combination of a dovish tone from the Federal Reserve despite doubling the tapering, Santa Claus rally and signs the new COVID variant – while spreading quickly – wasn’t as severe as feared. Of particular note is the wide dispersion within asset classes of US and international equities. US large caps outperformed small caps by over 10% as tech dominated large caps; international developed markets outperformed emerging by over 13%, or said more accurately, emerging trailed by 13%. Treasury rates continued the drift higher, causing 30-year treasury bonds to fall over 2% for December. TIPS and high-yield credit did quite well YTD. And how about those REITs and Commodities? REITs were the biggest surprise on the table.

Most asset classes have fallen during the first three days of 2022. Rates are a key driver.

I am showing the Growth v. Value chart again with a few observations. At the end of the year Growth outperformed by about 8%. The first three days of 2022 has erased 75% of that outperformance. Notice back in February when a similar thing happened. The common denominator – rising rates.

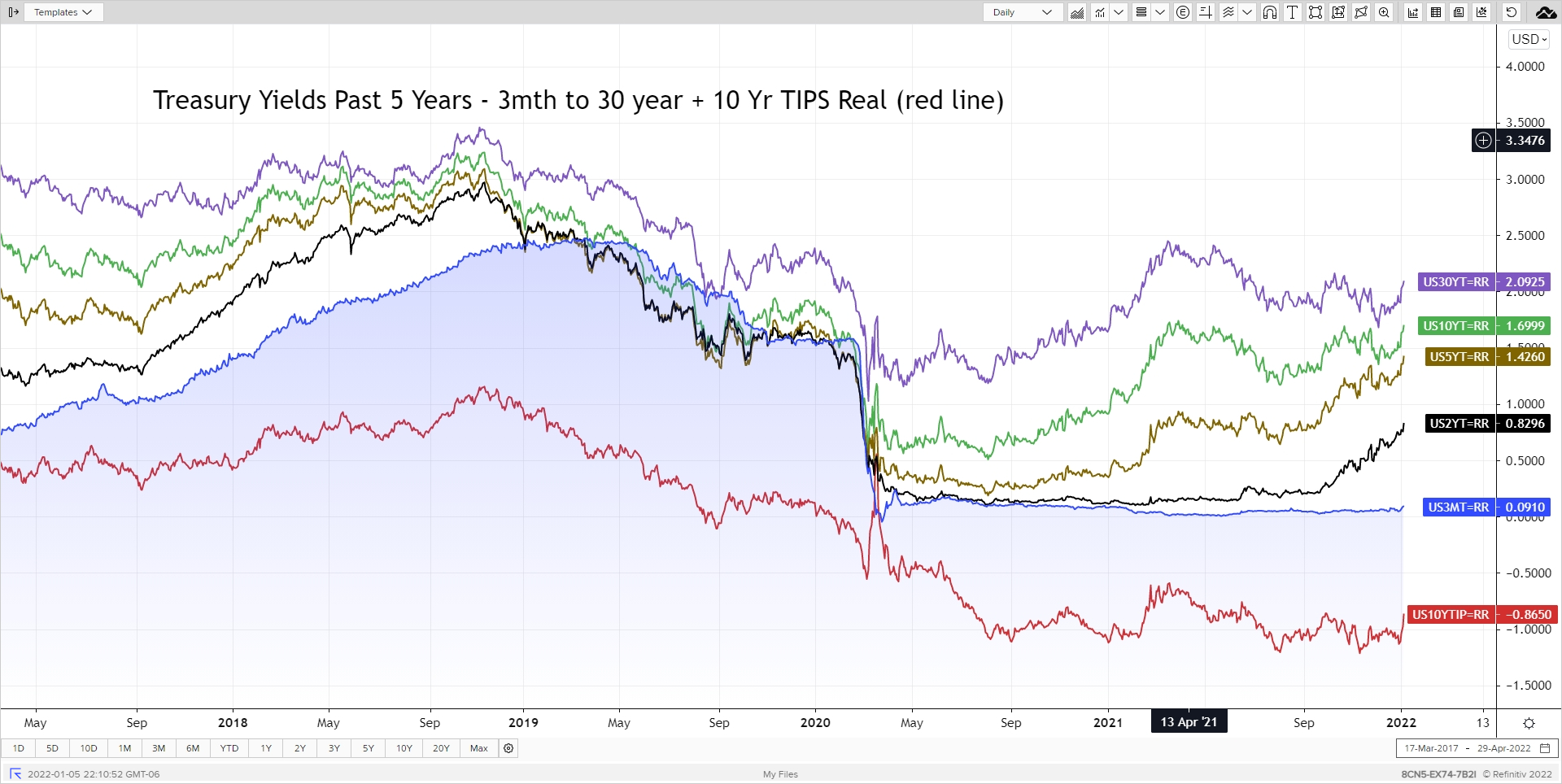

And here is that rate graph. Including the first few days of 2022, the 10-year is approaching the previous 2021 high while the 2- and 5-year never looked back. And unlike in early 2021, the 10-year real yield is not waiting around to join the rising rate party (becoming less negative). If this continues, it will likely hurt growth stocks more based on a higher, longer tail of earnings to discount. See my 2/28/2021 blog post for a detailed example of this concept.

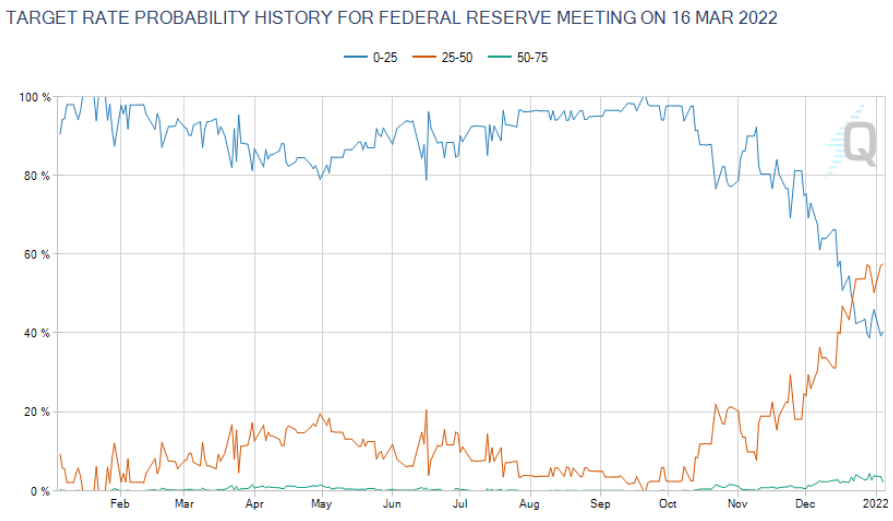

The Federal Reserve had a “productive” December meeting. The projections of expected rate hikes – captured by the dot plot – increased by 0.60% from the September projections. The Fed also announced a speeding up of bond tapering (slowing the $120 billion per month purchases by $30 billion per month instead of $15bb) so they can be done purchasing bonds by March 2022. This lays the groundwork for a potential rate hike as soon as the March 15-16 meeting. The Fed Funds market has begun to price in a strong possibility of that happening over this past month (Source: CMEGroup FedWatch tool).

Happy New Year! Make the most of it so you will know where the year went next December.

Posted by Kirk, a fee-only financial advisor who looks at your complete financial picture through the lens of a multi-disciplined, credentialed professional. www.pvwealthmgt.com