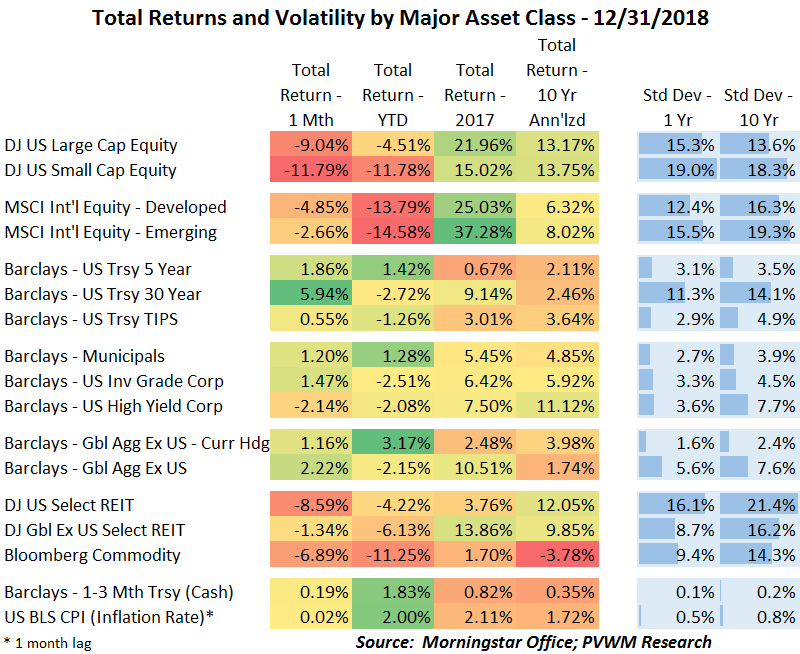

Asset Class Returns - 12/31/2018

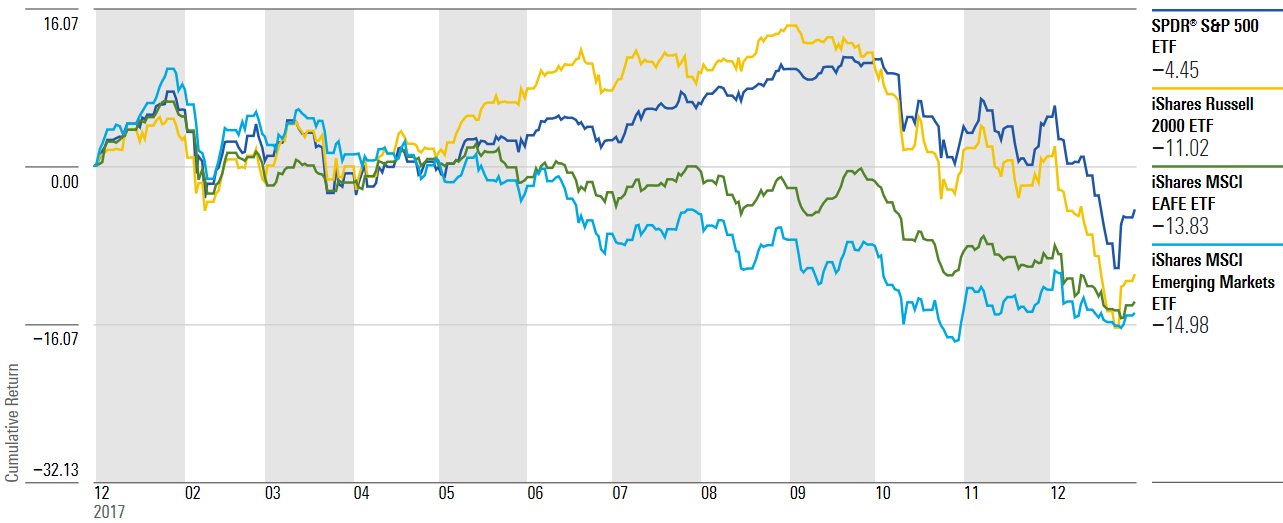

Should auld "indices" be forgot, And never brought to mind? ... That may have been the song many investors wanted to sing this New Year's Eve. US equity markets saved the worst month for last as December saw significant losses in the major indices. The same concerns persisted into the month, with global economic slowdown, trade negotiations with China and political issues on investors' minds. There was a significant shift in recessionary concerns driven by spillover from the global slowdown more than US activity at this point. The underlying economy remains strong but upcoming earnings and the more important future earnings guidance will be watched. All sectors were down over 4% in December, with Utilities holding up the best and Energy taking the bottom rung on both a month - down over 12% - and YTD basis, down about 18%. Health Care, Utilities and Consumer Discretionary were the only positive YTD return sectors. As a sign of 'risk-off', even US REITs were down substantially in December despite falling interest rates.

International equity markets ended the year with the worst YTD returns. However, much of their declines were incurred earlier in the year as global economies showed signs of slowing while the US remained strong. A strong US dollar also makes international holdings' returns lower in US $ terms. Valuations continue to remain attractive.

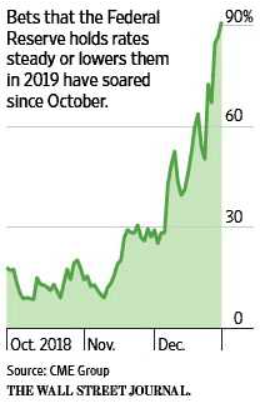

In addition to REITs surprising to the downside, the same two asset classes mentioned last month continued to drag - high yield and commodities. The concerns of an upcoming recession (I don't believe coming as soon) and continued drop in oil prices is adding to the high yield market concerns. And as ugly as the commodity returns look on a monthly and YTD basis, the more energy-heavy GSCI index was down even more. After the 10-year treasury rate hit 3.25% in early November, interest rates have been falling steadily since. Click here and scroll down to the second graph to see how much rates have fallen for all maturities except the 3-month T-Bills which was sporting a 2.40% yield at year-end. The last FOMC meeting of the year included an update to economic projections and the range of expected Fed rate hikes called the 'dot plot'. Relative to the September 'dot plot', the collective range of expected hikes was lowered from four hikes to three, though Fed Chair Powell continues to downplay the 'dot plot' significance in the follow-up press conference. The one thing that has stunned me over this past month is the shift in sentiment of the expected Fed rate hikes. The graph below from the WSJ provides the jarring picture. Happy New Year!