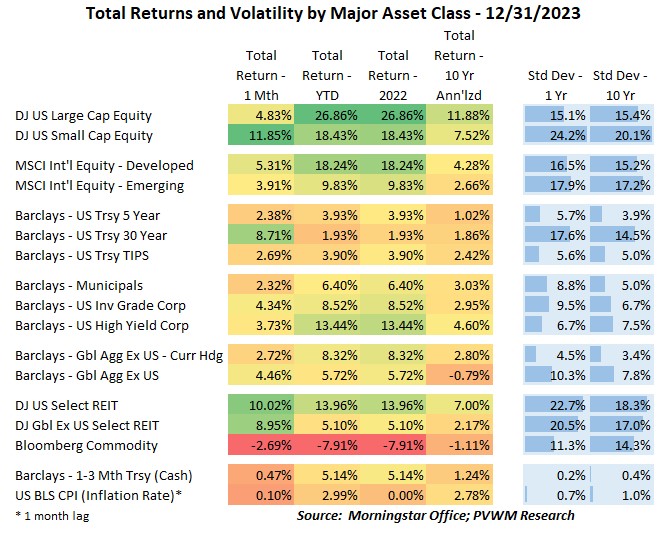

Asset Class Returns - 12/31/2023

The month of December continued the extremely strong performance seen in November. Monthly returns were similar or slightly lower than November with one notable exception – US Small Caps were up close to 12% for December alone.

The drivers this month were similar to last month – not only dovish but a Fed pivot at Dec 13th FOMC meeting, more buyers than sellers of longer duration bonds as Treasury adjusted issuance plans to more T-Bills, and favorable inflation readings. The November jobs report was also quite solid. The market viewed this information as further evidence of avoiding a recession and achieving a soft landing. There is also the potential a continuing strong jobs market could keep inflation higher and therefore delayed cuts by the Fed, but the market put that in the “tomorrow worry” bucket.

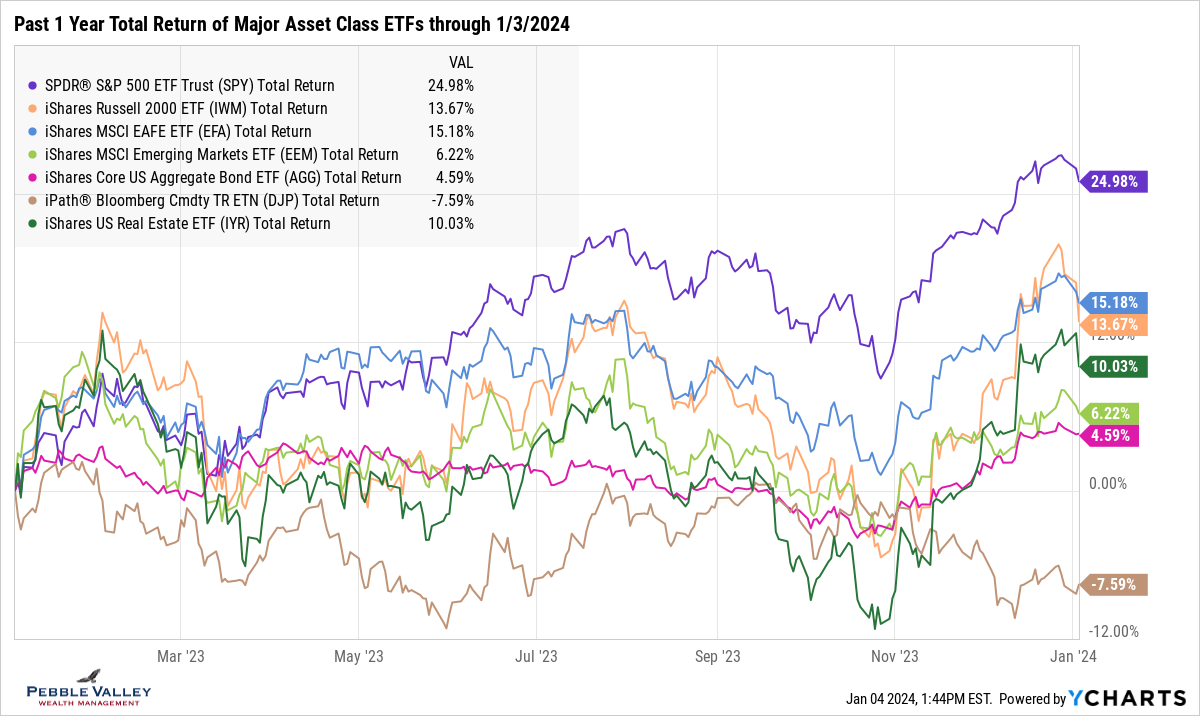

The graph below shows total returns of major asset class ETFs over the past year (total return includes reinvested interest and dividends). I include the first two days of 2024 as the market is experiencing a cooling off from the red-hot last two months of 2023. The relative peak of 12/31/23 reminds me of the last relative peak of 7/31/23. Back then there was a strong run in returns on the back of easier Fed expectations, only to reverse course over the next few months. This latest rally also started on expectations of Fed cuts, with an added boost in mid-December after the surprising Fed pivot. This was most pronounced in US Small Caps (orange line) and REITs (dark green line). These are also the two asset classes falling the most in these first two days of the new year.

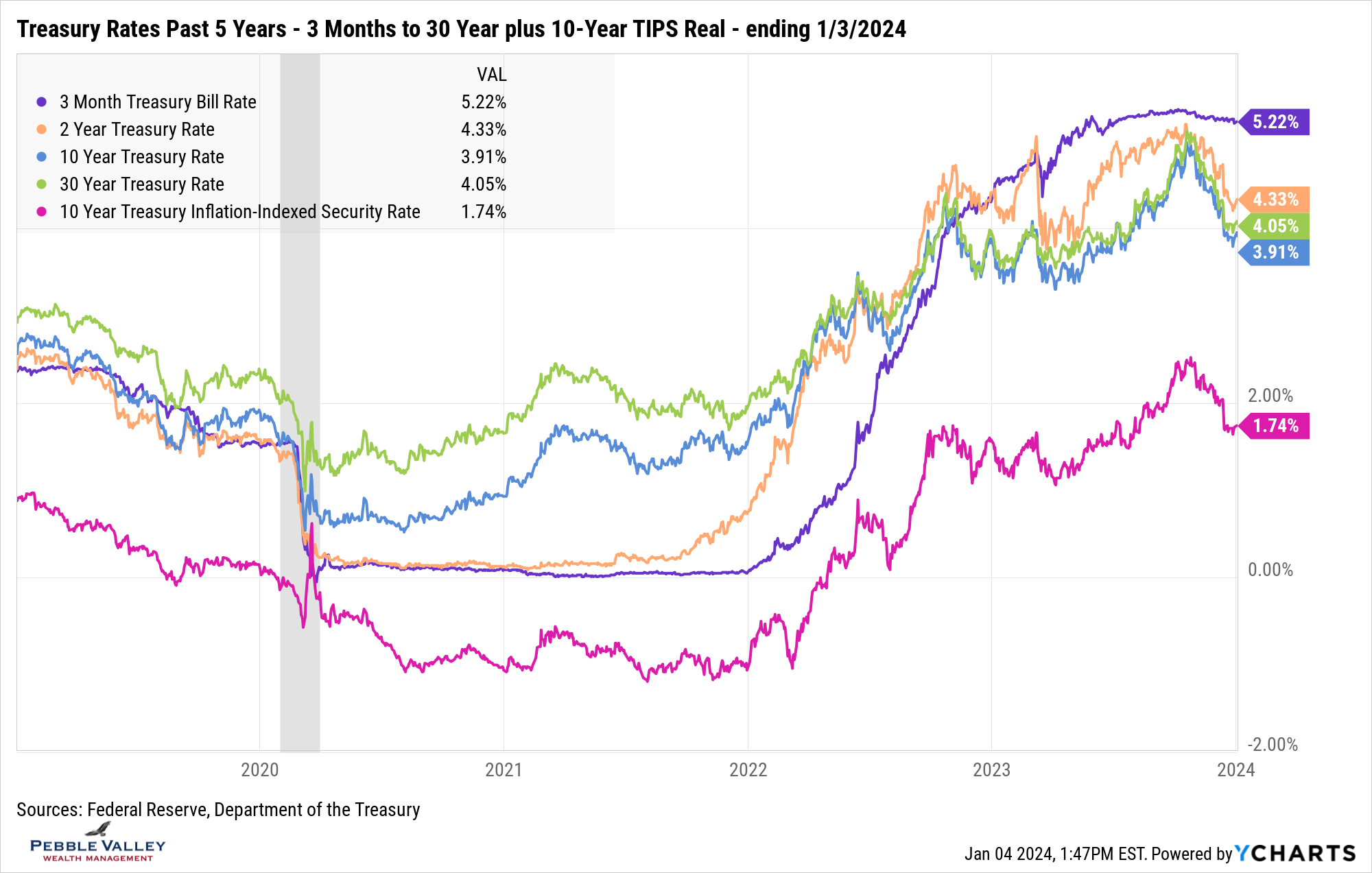

Treasury rates continued their march lower, reversing the large run-up in rates started in early August after the Treasury announced additional funding needs to cover the larger deficit. With the exception of the 2-year rate, the key rates are back to end of July levels. It is hard to see on the graph with 5 years of history, but similar to the equity rally cooling off, the first couple days of 2024 are seeing rates tick higher. Even real yields (from TIPS market) saw a big pullback in rates, which should be sustained if inflation readings continue to drift lower.

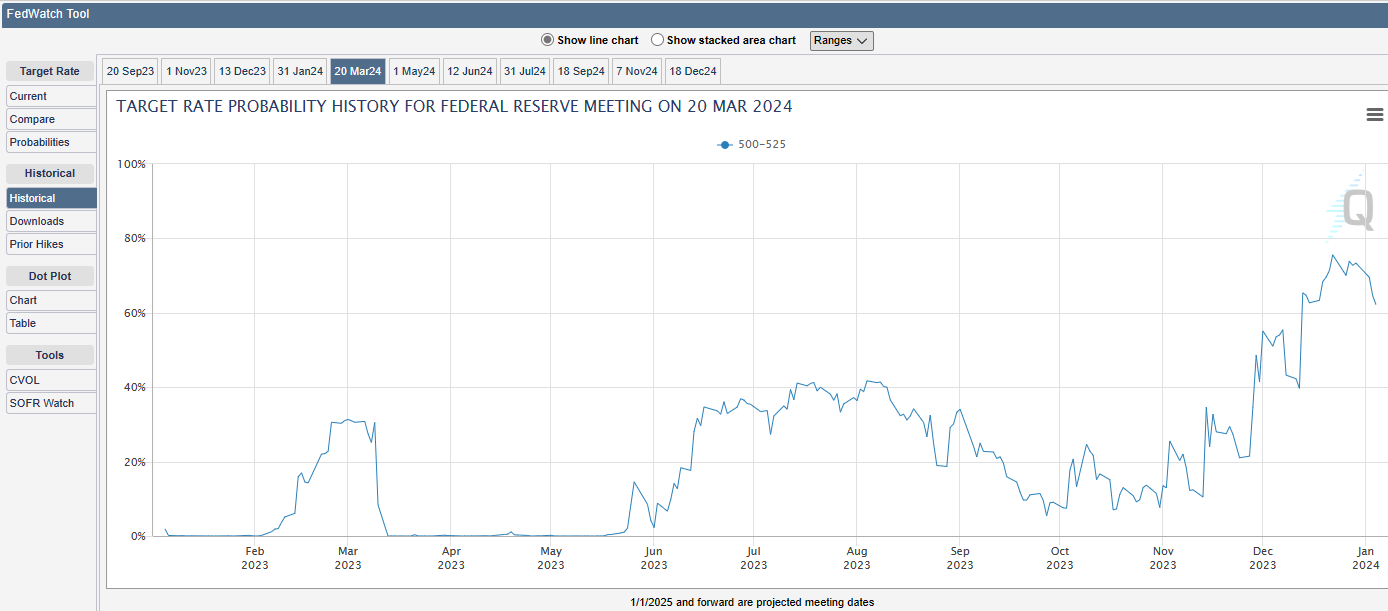

The latest FOMC meeting concluded December 13th. There was no rate change as expected, but the surprise came from the Summary of Economic Projections (SEP) and the press conference that followed. The market had begun to price in multiple rate cuts during 2024. The SEP showed a surprising three rate cuts or a total of 0.75% reduction in Fed Funds rate by the end of 2024 vs. the September expectation of only one rate cut. The inflation expectations were revised down slightly but unemployment was not. See Table 1 in this link for all the details. The press conference that followed was even more dovish, with Fed Chair Powell not pushing back at all on the market sentiment of more rate cuts sooner. This gave the bond market plenty of reasons to rally in price bring the yields down to the low levels mentioned above. With the benefit of the first couple days of 2024 and using the CME Fedwatch tool, Fed Funds futures began pricing in a very high probability of the first rate cut at the March FOMC meeting, but has since backed off from a 75% chance down to the low 60’s% the first couple days of this year. It still feels overdone to me.

The special topic this month is a brief reminder that active tax planning is a year-round thing, not just last-minute moves at the end of the year. Be aware of your marginal tax bracket at both the income and capital gains level, if on Medicare be aware of IRMAA, and be pro-active on funding or converting to tax qualified accounts. Call if need help.

Happy New Year.

Posted by Kirk, a fee-only financial advisor who looks at your complete financial picture through the lens of a multi-disciplined, credentialed professional. www.pvwealthmgt.com