Asset Class Returns - 11/30/2019

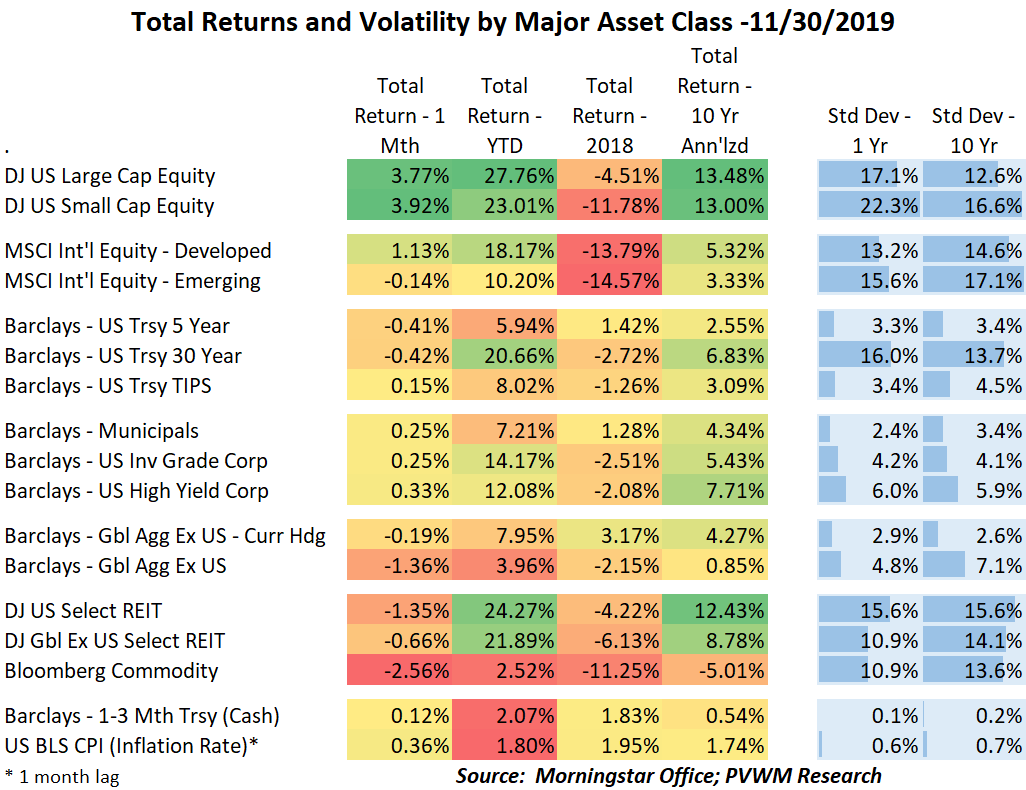

The month of November felt like a quiet month. Yet the equity markets kept chugging along with US large caps hitting an all-time high while small caps remain below their peak from last fall. At the sector level, Technology was the clear winner both over the past month and YTD. Financials have been picking up steam of late; Energy continues to lag. REITs and Utilities had the worst performance over the past month, down about 2%. For factor investors out there, High Quality stocks have the best YTD returns while Value stocks have picked up momentum (and fund flows, or is it the other way around?) over the past three months.

International equities continue to lag the US equity markets over past month (EM slightly negative) and YTD, but had a robust 3-months. Economic growth is much more sluggish outside the US which explains the drag on those markets. Recent economic data out of Europe has been more favorable and the trade winds have been blowing in a positive direction, but definitely swirling, which impacts markets. Commodities continue to lag as the dollar remains strong along with that sluggish global growth backdrop.

Rates were relatively flat to up slightly on the month. If you squint your eyes you can see corporate spreads – the extra yield received from investing in bonds riskier than treasuries – moved down slightly leading to the small positive gain for the month for corporate bonds. The overall high yield market – bonds from companies with more debt and greater chance to go bankrupt in a downturn – also showed a small positive return but the lowest rated CCC debt has been showing signs of weakness. For the bond geeks out there, you noticed the pop in repo rates in mid-September and subsequent Fed infusion of liquidity on the short-end. Here is a podcast that explains the inside workings of the key drivers to the stress.

Someone asked me recently where a person should invest if they want a defensive posture since it appeared everything was already quite lofty. It is a unique time in that almost all major asset classes have very solid YTD returns. But don’t forget the Christmas Eve lows from last year that serve as the starting point. The graph below shows total returns from the beginning of 2018. Yes the US large caps have recovered from the September 2018 high but not all. And that purple line – corporate bonds - have had very strong returns driven by low rates.

Posted by Kirk, a fee-only financial advisor who looks at your complete financial picture through the lens of a multi-disciplined, credentialed professional. www.pvwealthmgt.com