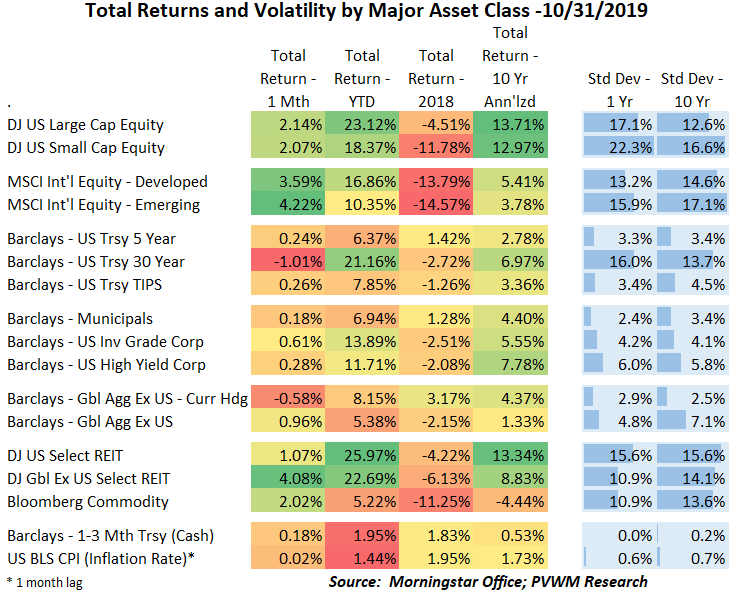

Asset Class Returns - 10/31/2019

How about that jobs report?

As the month of October began equity markets – US and international – were on a downward trend after hitting near relative highs from mid-September. The normally volatile month of October was ahead along with the usual suspects of worries on the economic and political stage. The September jobs report released early in October didn’t add to confidence.

Then the month unfolded. Quarterly earnings and guidance were more favorable than expected, trade negotiations on Phase 1 of the complex China deal continued to progress toward a likely signing in November and the Fed cut short-term rates as expected but also indicated they will likely be done for awhile unless economic data comes in different than expectations.

US equity markets posted another solid monthly gain, bringing large caps to an all-time high. US small caps also were on the march back toward the peaks but more ground needs to be made up. Volatility – as measured by the VIX – ended the month near the low end of the range over the past two years though staying above the crazy low levels of 2017. At the sector level, HealthCare and Tech were on fire with Financials and Communication close behind.

International equities and REITs were even stronger, rising 3.6% for developed markets to 4.2% for emerging. There are many moving parts and drivers captured in these returns, but key drivers were a delay in a hard Brexit as a plus for developed markets and favorable trade negotiations helping emerging. Emerging still lags US by a wide margin YTD but developed markets are catching up.

Rates began drifting up throughout the month but dropped back close to unchanged at month-end. Long-term (30-year) treasury rates did end slightly higher on the month. The high duration of long bonds caused even this slight rise in rates to result in a 1% loss for the month. However, holders of these bonds since January are still smiling. Commodities saw a bounce across the various sub-sectors, even energy.

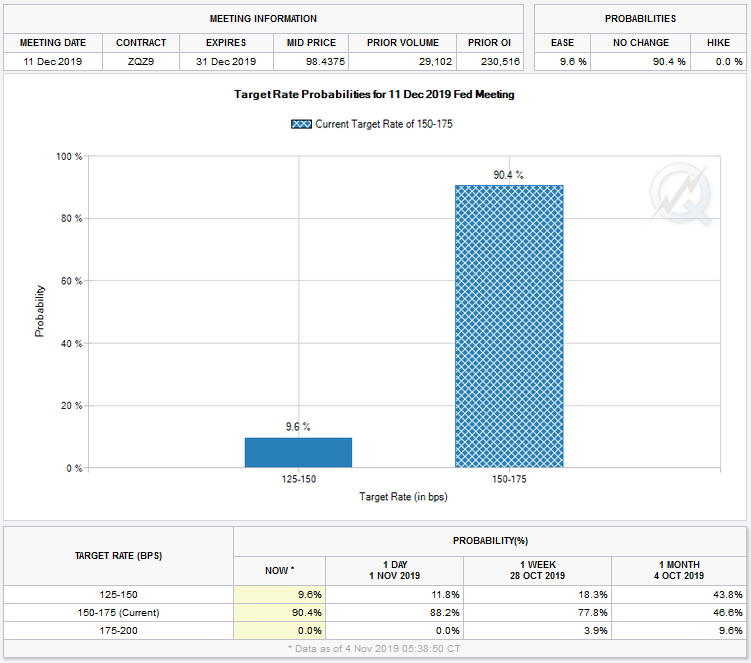

I end with two pictures capturing notable economic events during October. The first graph shows the Fed Fund futures market is pricing in a 90% chance the Fed does NOT lower rates again in December after the Fed statement on October 30. This implied % was as low as 47% just one month ago. The second graph shows not only the strong jobs growth this past month, but the previous two months were revised up by an additional 95,000 jobs. The current month change in jobs of 128,000 also included the impact of the GM strike which was estimated to decrease this number by about 40,000. Strong job growth continues to put money in consumers’ pockets to spend which continues economic growth.

Posted by Kirk, a fee-only financial advisor who looks at your complete financial picture through the lens of a multi-disciplined, credentialed professional. www.pvwealthmgt.com