Asset Class Returns - 05/31/2020

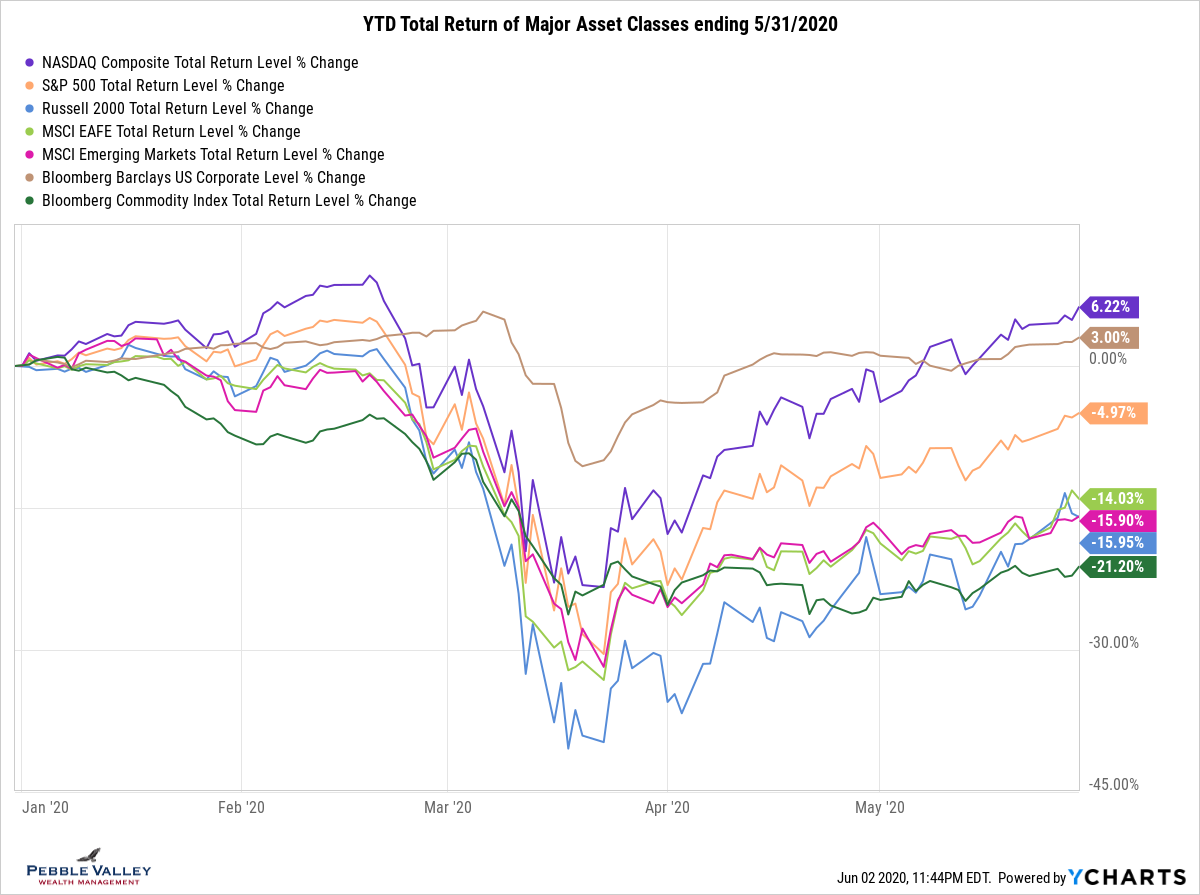

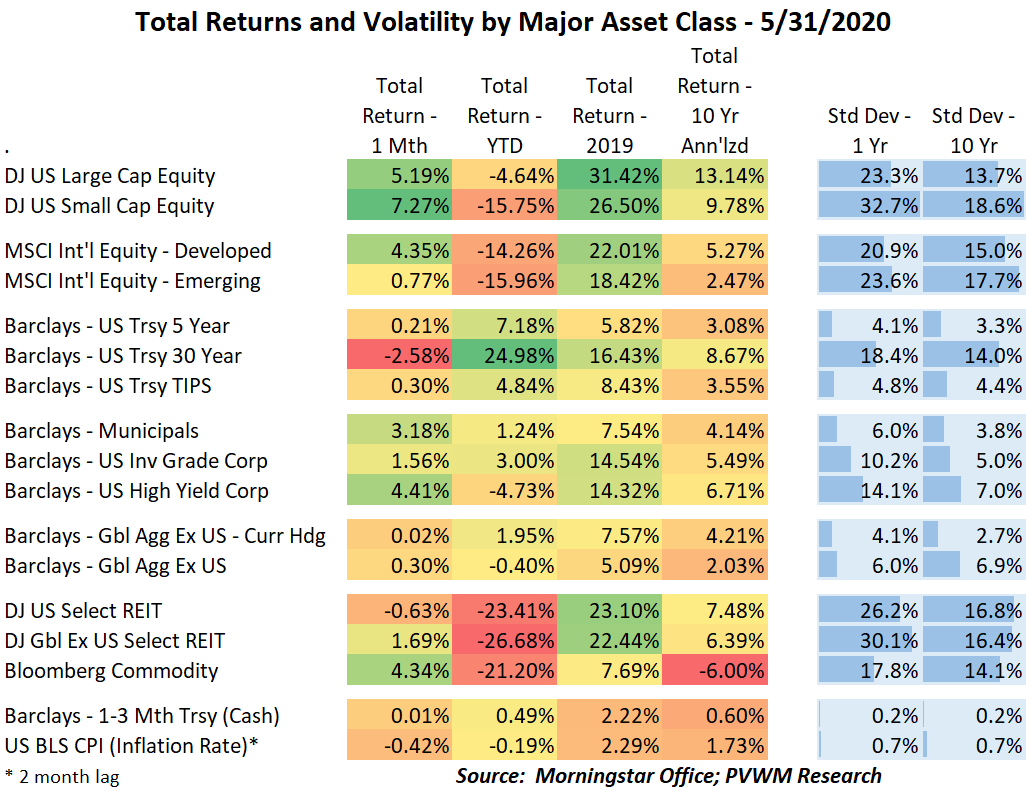

Not all the major equity markets behaved the same coming out of the lows of March 23. US large caps, helped by the technology sector, was pulled from the lows most quickly and is only a few percentage points from being flat on the year. I added the tech-heavy NASDAQ in the graph below to show its out-performance and explain part of the US large cap run. US small caps are lagging by a wide margin to large caps due to the smaller balance sheet being less able to withstand a revenue shock, though they too had a strong run at the end of this month. International equity is also lagging US large caps by a similar magnitude.

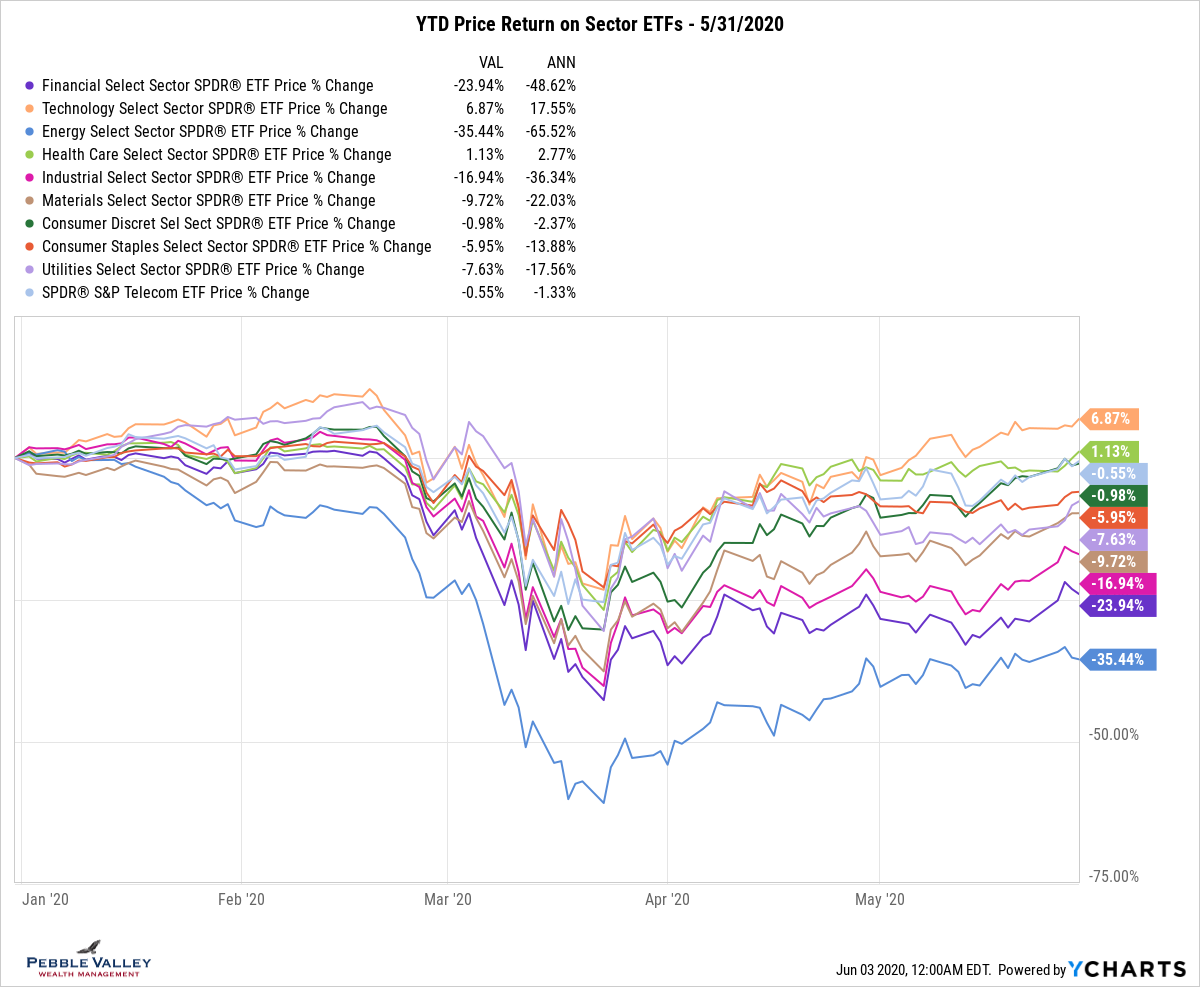

At the US sector level, Technology and Health Care lead the pack – even a positive return YTD - while Energy and Financials continue to be the worst performing sectors. This also explains a large portion of the relative performance of Growth over Value since each pair of sectors is in the respective group.

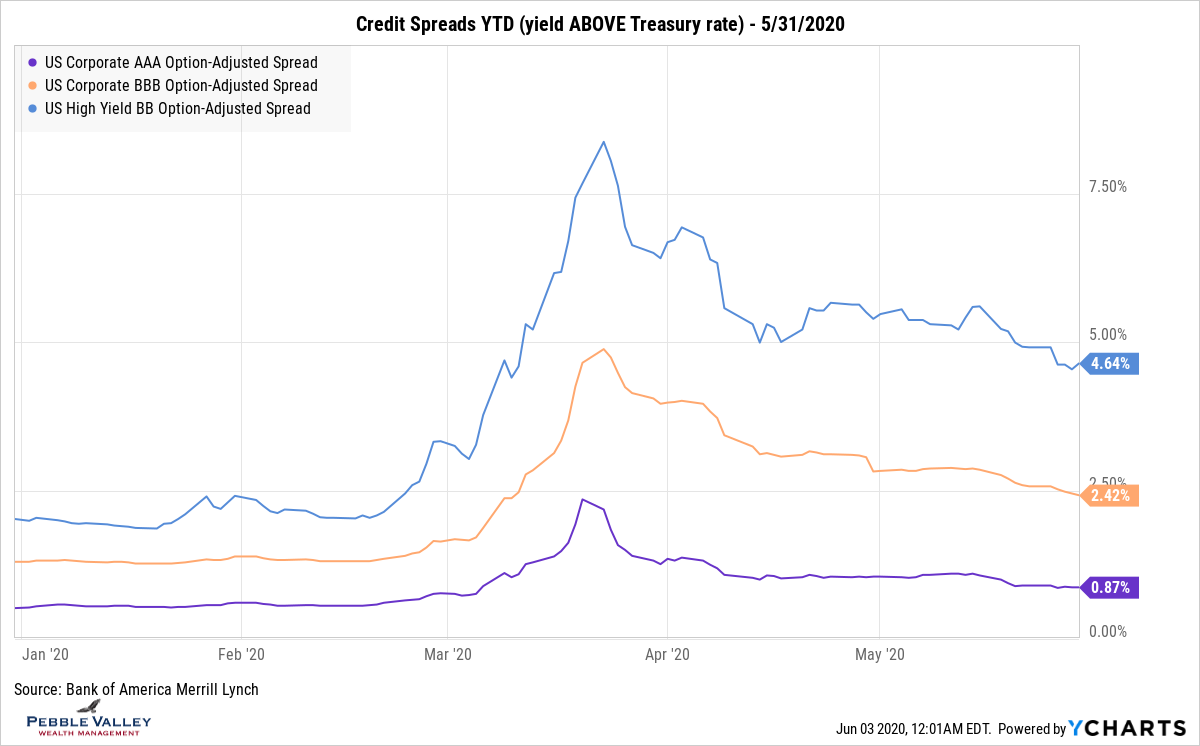

Treasury yields (and cash savings rates) remain near 0% on the short-end and below 0.75% on the 10-year. The 30-year is just under 1.50% but appears most vulnerable to ‘yield up/price down’. The extra yield investors receive to take credit risk blew out in late March but has been marching back in, though still wide from pre-COVID levels. The Fed has been shooting the money cannon at various parts of the bond market which has responded favorably. Muni’s finally had a good month in May after being left out of the initial “Fed buying party”. Only high yield had a better monthly return, though high yield in both corporate and muni’s remains negative YTD.

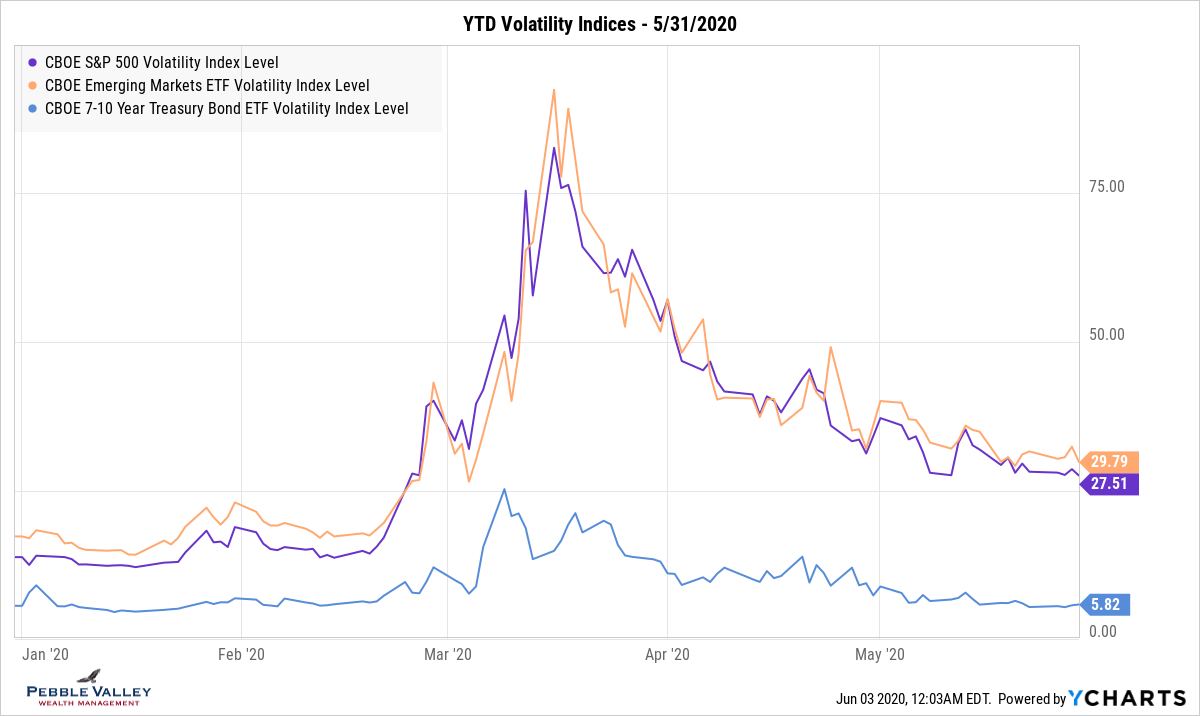

I will end on implied volatility. It is now finally below 30, barely. The go-go equity markets of late may make an investor feel a little complacent but this particular gauge remains elevated, though trending in the right direction. It also makes options remain attractive if you are a seller of the volatility.

Enjoy the equity run. Enjoy the warm sun. Enjoy the ice cream fun.

Posted by Kirk, a fee-only financial advisor who looks at your complete financial picture through the lens of a multi-disciplined, credentialed professional. www.pvwealthmgt.com