2024 Social Security Benefit Inflation Estimate: 3.1 – 3.3%

Each fall after the release of September CPI data the inflation adjustment for Social Security benefits is finalized. The final CPI-W data point will be released October 12th. Using the two known data points and assuming the index goes up anywhere from 0.00% to 0.60% for September, the result will be a 3.1 – 3.3% increase for Social Security benefits in 2024! The Medicare premiums for 2024 have not been finalized but are expected to rise to $179.80/month, currently $164.90. The extra Medicare premium surcharges (called IRMAA) have not been finalized yet but the MAGI income thresholds are expected to increase about 4% to $101,000 if single; $202,000 if filing jointly.

There is also an inflation adjustment that impacts current workers (based on a different index). The FICA tax includes both Social Security (6.2%) and Medicare (1.45% +). While the Medicare tax is applied to all income, there is a cap on Social Security which is adjusted based on wage inflation. While not finalized, it is expected the maximum earnings subject to the 6.2% FICA will rise about 4.7% to $167,700, resulting in an extra $465 taken from your paycheck over the year if income is above those levels, double that if self-employed. See the end of this post for more details.

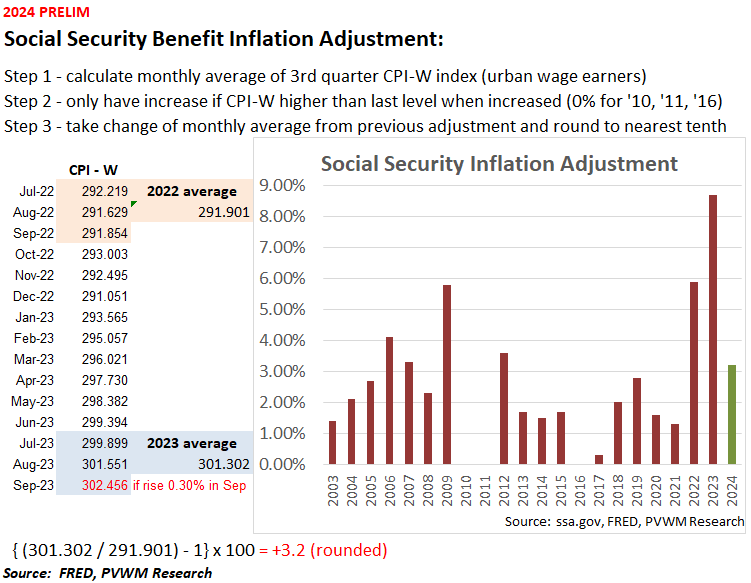

How is the SS benefit inflation adjustment determined?

The graphic below shows the steps to calculate the inflation adjustment and a graph of actual increases since 2003. A 3.2% increase is well below the last two years, but remains above average.

Different Inflation Indices

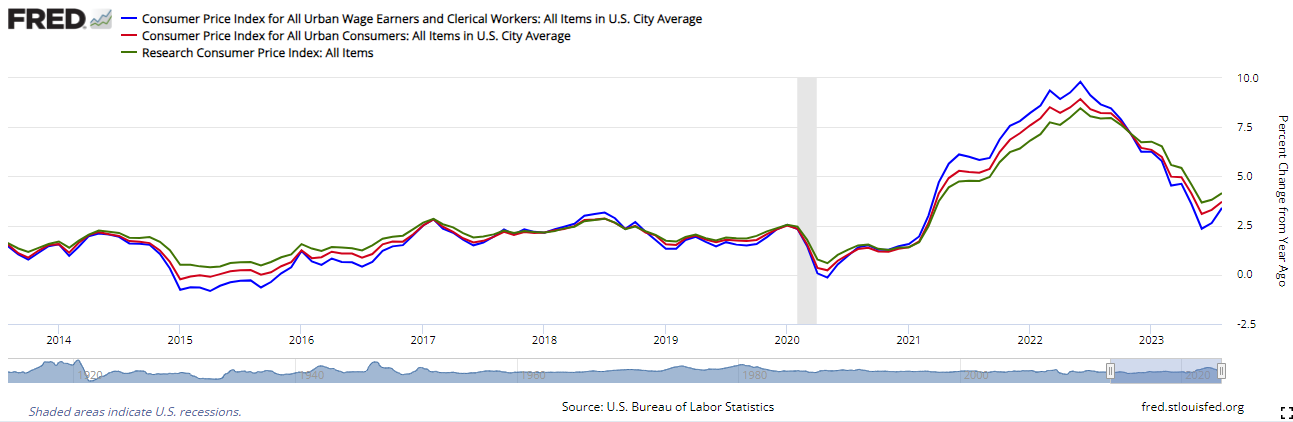

Note the inflation index used for Social Security benefits is the non-seasonally adjusted index for wage earners (CPI-W, blue line below), not the more common seasonally adjusted index for all urban consumers (CPI-U, red line) reported in the media. There is also a Research Consumer Price index (green line) which captures the common basket of goods and services for those age 62+. There are years when the 62+ index can diverge significantly from CPI-W, mostly in years when there is a large move up or down. From 2017 through early 2020 the Research Consumer index (62+) was nearly identical to the others. It was about 1% higher in the spring of 2020, then lagged noticeably the last couple years and is now higher again. While the voices demanding the use of the 62+ index were silent during the last couple years’ high adjustments, they may become louder again. Just keep in mind the long-term trends, and the recent bumps in your favor. The graph below shows these indices over the past ten years (Note: shaded area is for recession).

Current workers’ impact on FICA taxes

For those working and paying into Social Security (6.2% payroll tax for SS on wages up to $160,200 for 2023), the estimated increase in wages subject to this tax is based on a different index – the ‘national average wage index’ – calculated by Social Security. Recall there is an additional 1.45% payroll tax for Medicare that is applied to all wages (not capped), plus an additional 0.90% on earnings above $200,000 for individuals and $250,000 if married filing jointly (NOT indexed to inflation!). Your employer also pays these taxes (or you if self-employed), except the extra 0.90% which is only paid by you.

Check out my recent SS blog post for a deeper dive into the Social Security and Medicare financial status. Yes, it will still be there for the concerned young workers, but expect a roughly 20% haircut if no Congressional action is taken – based on the 2023 Trustee report and if you combine the “Disability Insurance (DI)” fund along with the “Old-Age and Survivors Insurance (OASI)” fund.

Similar to higher IRMAA thresholds mentioned above, there are other inflation adjustments that will occur for IRS tax brackets, standard deductions, estate tax exemptions and other items. The IRS will publish these later. Note however these will apply for the 2024 tax year, not the current year where those values are known and should be used for active tax-planning. If not engaged, give us a call.

Enjoy the expected raise if receiving benefits; thank you for your added contributions if still working and making more than $167,700 for 2024!

Posted by Kirk, a fee-only financial advisor who looks at your complete financial picture through the lens of a multi-disciplined, credentialed professional. www.pvwealthmgt.com